The top 100 angel investors by number of deals in 2025 include the most active individuals globally, many of whom have hundreds of investments each and a proven record of backing high-growth startups. Here is a structured overview of the most frequently cited names, emphasizing those recognized for their deal count and broad startup impact:rocketdevs+1

Most Active Angel Investors (Top 30 by Deal Count)

Name

Estimated Deals

Notable Investments

Ron Conway

600+

Google, Facebook, Airbnb

Gil Penchina

300+

LinkedIn, PayPal, AngelList

Dave McClure

500+

Twilio, SendGrid, Lyft

Naval Ravikant

200+

Twitter, Uber, Stack Overflow

Mark Cuban

200+

Box, Uber, Snapchat

Jeff Clavier

200+

Fitbit, Eventbrite, SendGrid

Brad Feld

200+

Fitbit, Zynga, MakerBot

Josh Kopelman

200+

LinkedIn, Uber, Squarespace

Keith Rabois

200+

YouTube, Airbnb, Palantir

Aydin Senkut

200+

Shopify, Rovio, LendingClub

Fabrice Grinda

200+

Alibaba, Airbnb, FanDuel

David Cohen

200+

Uber, SendGrid, Twilio

Paul Graham

200+

Dropbox, Airbnb, Stripe

Alexis Ohanian

150+

Instacart, Zenefits, Wayup

Gary Vaynerchuk

150+

Uber, Twitter, Venmo

Jason Calacanis

150+

Uber, Thumbtack, Calm

Reid Hoffman

150+

Airbnb, Facebook, Zynga

Dave Morin

150+

Nest, Venmo, Meerkat

Other Prominent Angel Investors (Sampling from Top 100)

Joanne Wilson (100+) — Food52, Catchafire, Lover.ly

Tim Ferriss (50+) — Uber, Facebook, Twitter

Ashton Kutcher (60+) — Airbnb, Uber, Spotify

Max Levchin (100+) — Yelp, Pinterest, Evernote

Matt Ocko (100+) — Facebook, Zynga, Lending Club

Jeremy Liew (100+) — Snapchat, The Honest Company, Affirm

Steve Anderson (100+) — Instagram, Twitter, Heroku

Mike Maples Jr. (100+) — Twitter, Okta, Cruise

This list compiles those most recognized for the highest deal volume—not just their personal profile—ensuring a global, industry-spanning perspective. The complete top 100 list sources from key directories and market trackers and can be found via prominent databases like RocketDevs, Eqvista, and annual roundups from industry-focused sites.rocketdevs+1

For more detail, refer directly to these industry lists to access the ranked, regularly updated full 100 investor names and their detailed portfolio highlights.eqvista+1

Perplexity AI has rapidly emerged as a leading player in the AI-powered search engine market, disrupting traditional search paradigms with its innovative answer engine and aggressive growth strategy. Founded in 2022 by a team of AI experts, Perplexity has achieved remarkable growth, processing over 780 million search queries in May 2025 and reaching $100 million in annual recurring revenue. The company’s valuation has surged to $18 billion, reflecting strong investor confidence and market adoption. This report provides a comprehensive analysis of Perplexity’s business model, its competitive advantages, and the factors driving its outperformance relative to peers.

Company Overview

Perplexity AI, Inc. is an American privately held software company that offers a web search engine leveraging large language models (LLMs) and real-time web search capabilities. The platform synthesizes responses to user queries, providing concise answers with inline source citations. Perplexity’s products are designed to bridge the gap between conventional search engines and AI-driven chat interfaces, offering a more efficient and accurate way to consume and share information.research.contrary+1

Business Model

Perplexity’s business model is built on a freemium structure, with a free public version and a paid Pro subscription. The Pro subscription, priced at $20 per month, offers access to more advanced language models and additional features. The company also generates revenue through advertising and a new publisher revenue-sharing program, which supports media organizations with revenue sharing, access to APIs, and free Enterprise Pro for employees.digiday+2

Year

Revenue (Millions)

Monthly Queries (Millions)

Active Users (Millions)

Valuation (Billions)

2022

0

0

0

0

2023

1

0

0

0

2024

20

230

0

1

2025

100

780

22

18

Competitive Advantages

Perplexity’s competitive advantages stem from its unique answer engine, which combines LLMs with real-time web search to provide accurate, up-to-date, and cited responses. The platform’s focus on accuracy and transparency addresses the challenges of misinformation and AI hallucinations prevalent in other AI-driven search engines. Perplexity’s answer engine conducts real-time web searches to fetch the most current information, ensuring that current data takes precedence. Additionally, the engine cross-references model output with contemporary sources to verify accuracy and reliability.wikipedia+1

Perplexity offers several focus modes tailored to specific content types or user intents, including ‘Web’ for general-purpose search, ‘Academic’ for peer-reviewed academic papers, ‘Social’ for online discussions and opinions, and ‘Finance’ for searching SEC filings and earnings calls. Users can toggle between these modes directly in the interface, enabling more relevant results for queries ranging from scientific research to community opinions.research.contrary

Market Performance

Perplexity’s market performance has been exceptional, with a 400% year-over-year revenue growth from $20 million in 2024 to $100 million in 2025. The company’s monthly search queries have surged from 230 million in August 2024 to 780 million in May 2025, demonstrating increasing adoption as users seek alternatives to traditional search engines. Perplexity’s active user base has grown to 22 million, and the company holds a 6.2% market share in the AI search market as of 2025.taptwicedigital+1

Strategic Initiatives

Perplexity’s strategic initiatives include the launch of its Comet browser, which represents a fundamental shift in how AI interacts with the web. Comet leverages “agentic search” to perform complex tasks like booking flights, managing online purchases, and filling forms with minimal user input. The browser employs a sophisticated hybrid architecture that balances on-device processing using lightweight neural networks for basic tasks with cloud-based resources for more complex operations, automatically switching between modes based on network latency, model size requirements, and data sensitivity.perplexity

Perplexity’s Comet browser also integrates WebML API for hardware-accelerated operations, model caching, and a privacy sandbox that processes sensitive inputs through isolated Web Workers. This architecture enables AI agents to bypass platform restrictions and seamlessly integrate with various applications. With over 800 app integrations planned, Comet aims to become a central hub for digital interactions while prioritizing user privacy through local-only processing for sensitive operations, pseudonymous cloud interactions for non-sensitive tasks, and explicit consent requirements for data-intensive operations.perplexity

Competitive Landscape

Perplexity faces competition from established players like Google, Bing, and emerging AI search engines such as ChatGPT and specialized AI search tools. However, Perplexity’s focus on accuracy, transparency, and real-time web search gives it a distinct edge. The company’s aggressive growth strategy, strategic partnerships, and innovative product offerings have enabled it to carve out a significant market share in the rapidly evolving AI search landscape.taptwicedigital+1

Challenges and Risks

Despite its success, Perplexity faces challenges and risks, including legal scrutiny over allegations of copyright infringement, unauthorized content use, and trademark issues from major media organizations. The company’s use of undisclosed web crawlers with spoofed user-agent strings to scrape content from news websites has drawn criticism and legal action. Additionally, privacy advocates have expressed concerns about the potential for data collection, despite the company’s privacy assurances.wikipedia+1

Conclusion

Perplexity AI has established itself as a leading player in the AI-powered search engine market, driven by its innovative answer engine, aggressive growth strategy, and focus on accuracy and transparency. The company’s business model, competitive advantages, and market performance position it well for continued success in the rapidly evolving AI search landscape. However, Perplexity must navigate legal and privacy challenges to sustain its growth and maintain user trust.research.contrary+3

This report provides a detailed analysis of Perplexity AI’s business model, competitive advantages, and market performance, highlighting the factors driving its outperformance relative to peers. The company’s innovative approach to AI-powered search and its strategic initiatives position it as a key player in the future of information retrieval and digital interaction.taptwicedigital+3

Reaching agreement in a joint venture partnership for business involves structured negotiation, legal diligence, and written documentation to ensure all parties’ interests are protected and the venture operates smoothly. The process typically includes several key stages, which are outlined below.sirion+3

Steps in the Joint Venture Agreement Process

Initial Discussions and Strategic Alignment: Parties engage in exploratory talks, confirm compatibility, assess mutual goals, and establish the purpose of the joint venture.phoenixstrategy+2

Term Sheet / Letter of Intent: Negotiation of a non-binding term sheet sets out core commercial terms, such as structure, contributions, profit-sharing, and governance, providing early consensus on major issues.stpetelawgroup+2

Due Diligence: Each party investigates the financial health, capabilities, and reputation of the others to identify potential risks and confirm suitability for the venture.sirion+1

Drafting the Agreement: Legal counsel, typically from one side, prepares the initial detailed draft of the agreement based on the term sheet and earlier discussions.phoenixstrategy+1

Negotiation: Both parties and their advisors negotiate and refine the draft, addressing points such as management structure, voting rights, funding obligations, intellectual property, and exit strategies.maccelerator+1

Legal and Financial Review: Independent legal review is essential for each party. Financial experts analyze contributions, profit/loss sharing, and tax implications to ensure the agreement meets business goals and legal requirements.stpetelawgroup+1

Execution: Once all terms are agreed upon and reviewed, authorized representatives sign the agreement, making the joint venture legally binding.sirion+1

Key Components of a Joint Venture Agreement

Capital Contributions and Equity: Details of each party’s financial and non-monetary contributions, ownership percentages, and provisions for additional funding.maccelerator+1

Management and Governance: Clearly outlined authority, responsibilities, voting rights, decision-making processes, and board/committee structure.phoenixstrategy+1

Profit and Loss Sharing: Defined formula for profit and loss distribution based on contributions or negotiated terms.phoenixstrategy

Intellectual Property: Explicit terms regarding existing IP, co-developed IP, and protection of core technologies.maccelerator

Exit Strategies and Termination: Conditions for dissolving the venture, buyout options, asset division, and remedial measures in case of breaches.stpetelawgroup+1

Dispute Resolution: Procedures for arbitration, mediation, or legal action, as well as conflict management mechanisms.stpetelawgroup

Legal and Practical Tips for Successful Agreement

Seek experienced legal counsel for drafting, negotiation, and review to minimize risks and ensure regulatory compliance.sirion+1

Use clear, written documentation for every stage, from initial intent to final agreements, to avoid misunderstandings and protect all parties.stpetelawgroup

Identify risks proactively and build in remedies and contingency plans to handle potential disputes and breaches.maccelerator+1

By following this structured approach, joint venture partners can maximize the chances of a successful, mutually beneficial collaboration while minimizing legal and operational risks.sirion+3

Here are 50 actionable tips to help invest like the world’s most successful investors—distilled from the wisdom of Warren Buffett, Charlie Munger, Peter Lynch, Benjamin Graham, Ray Dalio, and more.

Invest within your circle of competence—know what you understand best.

Prioritize businesses with enduring competitive advantages.

Buy at a margin of safety—only invest when there’s a clear discount to value. investorsedge.cibc

Think long-term: decades, not quarters or years.

Focus on cash flows, not reported earnings or market hype.

Look for owner-operator companies with skin in the game.

Study management integrity and capital allocation skills.

Prefer simple, understandable business models over complex ones.

Don’t follow the crowd—avoid herd mentality.

Embrace market corrections as opportunities, not threats.

Diversify, but not excessively—be selective with your bets. investorsedge.cibc

Reinvest profits for compounding returns.

Don’t chase “hot tips” or fad stocks.

Separate emotion from decision-making—remain rational.

Carefully read company filings, earnings reports, and footnotes.

Seek companies with strong balance sheets and low debt.

Monitor for changes in competitive landscape or management.

Don’t overpay for growth—growth for its own sake isn’t value.

Factor in taxes, inflation, and fees to your investment equation.

Ignore daily market noise—focus on business fundamentals.

Buy when others are fearful, sell when others are greedy.

Use market volatility to your advantage, not as a reason for panic.

Study the investing greats and read their letters and biographies.

Be patient—great investments take time to bear fruit.

Keep learning: read widely about business, psychology, and history.

Look for high returns on invested capital and strong free cash flow.

Invest in what you use and understand—see Peter Lynch’s “buy what you know.”

Respect risk—don’t risk permanent capital loss for extra return.

Consider macroeconomic trends, but don’t let them dominate your thesis.

Write an investment thesis and revisit it regularly.

Rebalance your portfolio when warranted, not reactively.

Don’t let past mistakes deter you—learn and improve.

Let winners run and cut losers quickly.

Use index funds or ETFs for broad exposure when stock picking isn’t viable. investorsedge.cibc

Understand the impact of incentives and human behavior on markets.

Track insider buying and selling as a clue—not gospel—of conviction.

Assess customer loyalty and brand value.

Consult expert networks or industry insiders for “on the ground” insights.

Anticipate change, but don’t speculate wildly on what “could” happen.

Automate saving and investing for consistency and discipline.

Be humble—no one always gets it right.

Practice position sizing appropriate to conviction and risk.

Remember opportunity cost—sometimes the best action is no action.

Review your holdings for “thesis creep”—has your rationale changed?

Don’t let sunk costs bias hold you hostage in bad investments.

Read annual reports and investor presentations from competitors.

Assess global trends but don’t ignore local/regional context.

Network with other thoughtful investors for feedback and ideas.

Define your own investment objectives, risk tolerance, and time horizon.

This checklist reflects principles and strategies that underpin world-class investing success. Integrate them into your process for rational, long-term, and compounding gains. investorsedge.cibc

I just discovered this 22-year-old founder who built a $3+ million company in 60 days with just 1 employee and an army of college interns.

He is now a serious contender for the Lean AI Leaderboard with $4.4 M revenue/employee.

Meet Krishay Mukhija, the founder who started recruiting at 16 and turned childhood frustration into a recruitment revolution.

While most founders his age are still figuring out product-market fit, Krishay is serving 40+ enterprise clients, including Penn Medicine, Fortune 500 companies, and leading health systems.

The numbers:

$3+ million revenue in less than 60 days

40+ enterprise customers

1 core employee + 5-7 rotating interns

100% feature request completion rate

Sub-3-hour average resolution time

Built for the most compliance-heavy industries

This was no overnight success or lucky break. His advantage came from 6 years of obsession with recruiting automation, starting when most kids were playing video games.

Made $120,000 in 3 days at the age of 16

Krishay got his first job at a healthcare staffing agency. They handed him a cold list of 10,000+ nurses with outdated contact information and a simple instruction:

“Call every single person on this list until someone hits.”

The traditional approach was frustrating. He had to cold-call nurses who already received hundreds of calls weekly. Most numbers were dead and response rates were terrible.

Two days in, Krishay realized nobody picks up cold calls. So he shifted to texting first with researched, personalized messages. Better, but still painfully slow: 100 texts for 1-2 responses.

That’s when he built his first automation ever. It was not some sophisticated AI, just a simple script that moved his cursor around the screen:

The automation would type out and send personalized messages without him having to do anything.

He created 5 different text templates for different nurse profiles: recent retirees, California relocations, and career changers.

The script ran through his iPhone to send blue iMessages, bypassing expensive tools like Twilio.

Within three days, he reached all 10,000 contacts. 6 nurses were interested and placed. As a result, he made $120,000 in revenue.

It blew his mind, and since then, he has been obsessed with recruiting.

From VC Sourcing to Voice AI Breakthrough

That obsession led Krishay to General Catalyst’s Creation team, where he built LinkedIn automation tools to find hidden talent among founders. His scripts identified patterns like “Indian immigrant from University of Waterloo who’s worked at Databricks” as signals of future startup potential.

But the real breakthrough came in summer 2023 when he started experimenting with voice AI. Working with basic text-to-speech architecture, his team hit a milestone nobody expected: sub-1 second latency for the entire end-to-end process:

• Speech-to-text (transcribing what the candidate says)

• Text-to-text reasoning (AI coming up with a response)

•Text-to-speech (AI saying the response back)

That’s when he knew they had something special.

The Counterintuitive Customer Strategy

While most AI companies chase easy wins, his company Symbal AI deliberately targets the hardest customers: highly regulated organizations with compliance requirements who are naturally skeptical of AI.

He thinks someone who has an uneasiness of AI is the best client for Symbal AI because they built it from the ground up for safety and empathy. His co-founder had spent years building empathetic AI for veterans’ immersion therapy (use cases where saying the wrong word could cause real harm).

Their first paying customer was Penn Medicine, the largest employer in Philadelphia and the third most prestigious academic health system in the nation.

These are organizations that don’t adopt new technology lightly, yet they chose this 22-year old over established players. This speak volumes about his work.

The Three-Person Core + Intern Model

Symbal’s structure is deliberately lean but strategically leveraged:

Pranay (CTO and co-founder): Full-stack development and AI safety

Akash: Operations generalist who fills in all the gaps

Krishay’s work ethic and hustle are commendable. He reached out to me on LinkedIn, Twitter, email, and has a Calendly on for almost 12 hours/day, all 7 days of the week.

He took a call with me on the weekend and once late in the evening.

His Intern Strategy: 5-7 college interns at any given time, with 20+ total throughout their journey.

Every intern who joins Symbal recruits for 5 days to understand customer pain points firsthand.

He wants them to do 300 calls and have two people who are actually interested, because then they start understanding the value of 90-day attrition.

The training is intense but effective.

Clients regularly tell Krishay that their 19-year-old interns have an understanding that rivals that of a 27-year-old, 30-year-old, someone who’s been in the space for 5+ years.

The AI-First Operations Stack

Symbal runs entirely on automated workflows that would typically require entire departments:

Customer Success Automation:

Direct Slack/Teams channels with every customer

N8N workflows for automatic issue routing

100% feature request completion rate

Average resolution time: under 3 hours

Loom videos documenting every feature implementation

A visual representation of their n8n workflow for CSM management:

Talent Acquisition:

AI interviewing for all interns (including a Peter Thiel-branded persona for “zero to one” style interviews)

100-person applicant pools from single LinkedIn job posts

Focus on underwriting potential rather than pedigree

Sales and CRM:

Automated pipeline tracking through N8N workflows

AI-powered lead qualification

Automatic email, call, and interaction logging

They use customer success as a lever for product-led growth.

When sophisticated buyers request features, 80% of the time, other customers want the same thing.

The Compliance-First Technology Advantage

While competitors avoid regulated industries, Symbal built its entire stack for compliance:

SOC2 compliant data processing

NYC Local Law 144 compliant

Built-in bias detection and consistency guarantees

“Screen everyone, then choose the best” approach vs. resume filtering

Human-in-the-loop verification

Raw transcripts for compliance + intelligent summaries for usability

This compliance-first approach becomes a massive competitive advantage.

Krishay positions himself as a change management consultant helping recruiters prove that AI delivers better candidates and lower attrition rates.

The Client-Driven Product Philosophy

Symbal’s product development follows the radical principle: Clients are their chief product officers.

Instead of building in isolation, they create features directly from customer requests. The result is a 100% feature request completion rate, usually implemented within 3 hours.

This approach creates a powerful flywheel. Features requested by sophisticated buyers at Penn Medicine become selling points when talking to competing health systems. What looks like custom development actually scales across the entire customer base.

The Quality Over Quantity Hiring Philosophy

Symbal’s hiring philosophy centers on underwriting potential rather than traditional credentials. Every hire must have two spikes – two areas where they are exceptionally good.

This helps them find people who can learn quickly across domains. The ability to understand two different things deeply indicates strong learning velocity.

They deliberately hire from non-traditional backgrounds. While they have interns from Stanford and Princeton, they also have equally strong performers from Tennessee and Texas A&M.

The Hidden Leverage of Student Talent

College students provide massive leverage for Symbal, but not in the way most companies use interns. These students become sophisticated sales development representatives after just weeks of training.

The secret is that these students are native AI – they’ve been using AI since high school. Combined with intensive recruiting training, they develop genuine expertise in the customer’s problems.

The emotional impact is powerful as their customers love talking to young people who are solving problems that they’re passionate about.

The three-month rotation system ensures fresh energy while preventing burnout. Students work part-time around their studies, often making calls during lunch breaks.

The Revenue Model

Symbal’s revenue model is built for compound growth through phased implementations. Rather than one-time deals, enterprise clients start with one AI recruiting unit and expand quarterly.

Sample contract structure: $100k total value deployed as quarter one implementation, quarter two expansion, quarter three full rollout. This creates predictable recurring revenue while allowing clients to validate results before expanding.

Their revenue has two components: SaaS revenue and contractor revenue (immediate).

This approach generated $3+ million in revenue in less than 60 days, with clients including Penn Medicine.

The Future of Lean AI Companies

Symbal represents a fundamental shift in how AI companies can be built. Their success proves several counterintuitive principles:

Quality beats quantity: Three exceptional people plus a strategic intern outperform large traditional teams

Customer-driven beats feature-driven: Let sophisticated buyers guide your roadmap instead of guessing market needs

Industry expertise beats general AI: Deep domain knowledge in recruiting created authentic credibility and precise product-market fit

The Broader Implications

Krishay didn’t need venture capital because he was profitable from day one. He didn’t need a large team because AI handles routine work while humans focus on high-value activities. He didn’t need traditional sales and marketing because customer-driven product development creates organic word-of-mouth growth.

This model will likely become more common as AI tools become more powerful and accessible. The barriers to building software continue falling, while the leverage available to small teams continues rising.

The future belongs to founders who can combine deep domain expertise, AI-first operations, and obsessive focus on customer success.

If you’re building in this direction and want to accelerate your progress, I’m offering limited slots for 1:1 lean AI and/or founder advisory. DM me if interested

SpaceX Plans Tender Offer At $250 Billion Valuation | ZeroHedge

Elon Musk could be on his way to becoming the first trillionaire by the end of the decade, as two of his private companies soar in value, while his public company, Tesla, recently surpassed a trillion dollars in market capitalization.

A new report from the cites people familiar with the discussions, stating that Musk’s SpaceX–the world leader in rocket launches and high-speed space internet (via Starlink)–is preparing to launch a tender offer in December to sell existing shares at $135 each. This indicates that the rocket company’s valuation has surged by another $40 billion, reaching $250 billion, up from $210 billion earlier this year.

Starship rocket booster caught by tower pic.twitter.com/aOQmSkt6YE

— Elon Musk (@elonmusk) October 13, 2024

The people said Musk’s artificial intelligence startup xAI recently raised $5 billion at a valuation of $45 billion, doubling in just a few short months. Soaring values in Musk’s private companies have added to his overall net worth.

Musk’s cozy relationship with the Trump administration will likely result in Tesla winning the multi-year EV price war. A Reuters report from Thursday detailed how Donald Trump was planning to eliminate the $7,500 consumer tax credit for EVs. In return, this would destroy Musk’s competition, such as Rivian, Luicid, and legacy automakers.

As we previously noted, “Musk’s strategy to win the EV price war: Build the largest EV business with taxpayer dollars, popularize EVs, allow other startups and OEMs to enter the market, and then support politicians who want to end EV subsidies, crushing the competition and leaving Tesla reigning supreme.”

Meanwhile, ‘the Trump bump’ in equity markets sent Tesla shares over the trillion-dollar market cap level this past week.

According to the Bloomberg Billionaires Index, Musk’s net worth has risen to $306.5 billion, up $77.5 billion on the year – primarily because of the latest Tesla price surge.

In September, wealth-tracking website published a report forecasting Musk could become the world’s first trillionaire by 2027. This news is likely disheartening for struggling WeWork co-founder Adam Neumann, who famously said in 2019 that he wanted to live forever and become the first trillionaire.

Musk’s dominance in space, EVs, AI, and media–with no other billionaire even close to his level of success, and more importantly, to his contributions to the nation’s success in this global technology race–has only infuriated far-left, anti-American Democrats…

If you’re wondering how bitter the Left is at @elonmusk for trying to save America, Maddow is straight up demanding the Kamala administration (not gonna happen!) cancel all SpaceX govt contracts. Because “national security.” pic.twitter.com/kihdzhkAZS

— Buck Sexton (@BuckSexton) November 5, 2024

… who are now calling for the dismantling of Musk’s companies.

Elon Musk’s artificial intelligence company xAI is raising up to $6 billion at a $50 billion valuation, according to CNBC’s David Faber.

Sources told Faber that the funding, which should close early next week, is a combination of $5 billion expected from sovereign funds in the Middle East and $1 billion from other investors, some of whom may want to re-up their investments.

The money will be used to acquire 100,000 Nvidia chips, per sources familiar with the situation. Tesla’s Full Self Driving is expected to rely on the new Memphis supercomputer.

Musk’s AI startup, which he announced in July 2023, seeks to “understand the true nature of the universe,” according to its website. Last November, xAI released a chatbot called Grok, which the company said was modeled after “The Hitchhiker’s Guide to the Galaxy.” The chatbot debuted with two months of training and had real-time knowledge of the internet, the company claimed at the time.

With Grok, xAI aims to directly compete with companies including ChatGPT creator OpenAI, which Musk helped start before a conflict with co-founder Sam Altman led him to depart the project in 2018. It will also be vying with Google’s Bard technology and Anthropic’s Claude chatbot.

Now that Donald Trump is president-elect, Musk is beginning to actively work with the new administration on its approach to AI and tech more broadly, as part of Trump’s inner circle in recent weeks.

Trump plans to repeal President Joe Biden’s executive order on AI, according to his campaign platform, stating that it “hinders AI Innovation, and imposes Radical Leftwing ideas on the development of this technology” and that “in its place, Republicans support AI Development rooted in Free Speech and Human Flourishing.”

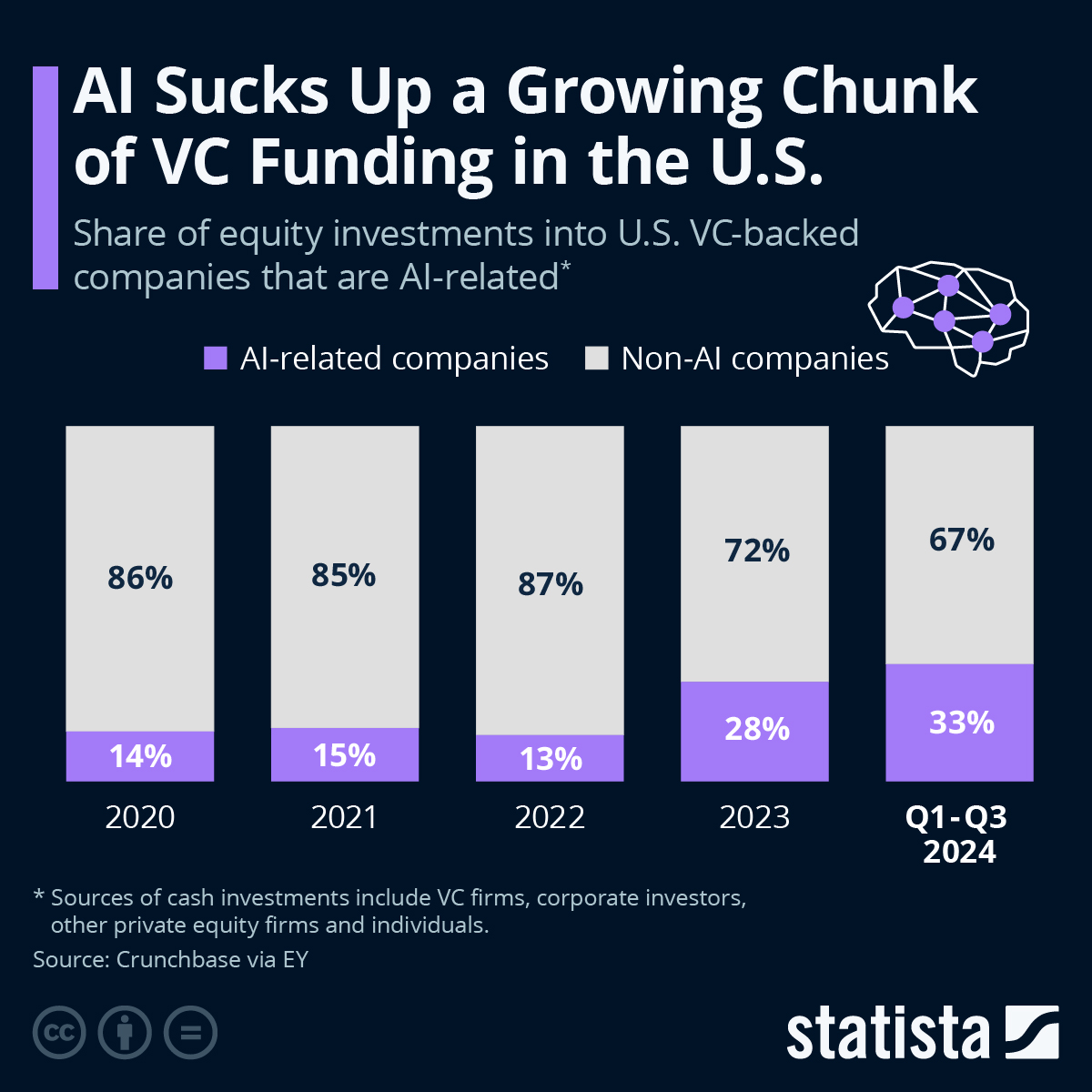

AI Sucks Up A Growing Chunk Of VC Funding In The US | ZeroHedge

Even more so than usual, San Francisco will be the epicenter of the world’s startup scene this week, as founders, investors and other industry insiders come together at TechCrunch Disrupt, one of the leading events of the startup scene.

Unsurprisingly, AI will take center stage at this year’s conference, as investors are looking for opportunities to invest in the booming, yet still nascent field and founders of AI-related companies will do everything to profit from the AI boom and secure fresh capital for their ventures.

As Statista’s Felix Richter shows in the chart below, AI has sucked up an increasingly large chunk of VC funding in the United States in recent years.

In the first nine months of 2024, AI-related investments accounted for 33 percent of total investments into VC-backed companies headquartered in the U.S. That’s up from 14 percent in 2020 and could go even higher in the years ahead.

According to Crunchbase data analyzed by EY, AI deals accounted for 37 percent of the $38 billion raised by VC-backed companies in Q3 2024, with four of the 10 largest deals involving AI-related companies.

The latest increase in AI-related investments is still expected to be just the beginning of a longer-term trend.

As EY notes in its latest report on VC investments, most of the funds funneled into the field are currently focused on building the foundation for the technology, e.g. developing and training AI models.

Once this wave of investment ebbs, entrepreneurs will need to figure out ways to actually utilize the potential of AI, which will likely kick off a second wave of AI investments.